You sit on the bed looking at the shoes on your feet, the BCBG platforms you just bought this afternoon at Nordstrom, and sigh because the left one already has a small scuff on the side from when you were waiting in line at the club. It's not in your character to get overly upset about a small scuff on new shoes, but you're embarrassed by how hard it is to fight back tears. You quietly cry on the edge of your bed, alone, because there is a scuff on the left side and now you can't even take them back.It's 2am, rent is due tomorrow and you can't...even...take...the...shoes...back.

Whether it was the extra appetizer you bought at dinner, the cover charge you ended up having to pay even though your best friend said you two would get in for free, or the fact that you had to spring for the $20 cab ride home because your girl lost her wallet in the bathroom, the point is now you have now spent you last dime and you have no idea how the heck you are going to finish out the month, let alone get to work on Monday.This my friends, is the picture of a financial meltdown. I know this story—in vivid detail—because this was a reality in my life not to long ago. The good thing about hitting rock bottom though, is that from there the only way out is up. The problem with up, however, is that such a direction is not always so obvious. Like a fighter pilot maneuvering his plane backwards, sideways, and upside-down, sometimes the only way to be sure we're head for the sky and not for the ground is by focusing on our map (i.e. plan) and not on our outside surroundings. Though the map to financial diligence will show a long, hard, road riddled with necessary stops in between, here were the first "stops" on my "map" that helped me get a handle on my financial life, immediately:

- Understanding My Problem(s)

- Tracking My Money

- Saving 10%

***

Understanding My Problem: "I haven't checked my bank account in 3 weeks because I'm too scared to look"

Before you can get started on rectifying your problem, you have to know where your problem lies. Since it's hard to fully be honest about what we're really bad at when it comes to money, I find that looking at your irrational behaviors when it comes to money are great clues about what your issues are. For instance, I was The Queen of not checking my bank account for weeks at a time because I was literally too scarred to look. Even though I knew good and well that I had severe issue with money, I spent years lying to myself (and everyone else) about my financial issues. The proof, however, was in my very real inability to spend 30 seconds checking my bank account every few days. If you asked me why, the answer was easy—"I'm scared to look because I might be sick when I see how much money is left in my account".

There are only two types of people who are constantly scared to look at their bank accounts for fear of a lack of funds: people who overspend because they have no self control and people who don't keep track of their money. I was both. So in short, if you want to find out what your deepest issues with money are but you fear you might not be honest with yourself, look at the irrational things you do when it comes to money. Crazy behavior with money shines an accurate light on who we are financially, every time.

Tracking My Money: "I can't believe I spend that much eating out!"

By now, you may acknowledge that you have issues with money, but you may think there's nothing you can do about it until you make a respectable salary. For years, I had this kind of thinking too; I convinced myself that if I just made more, all of my issues would go away. That all change when I heeded the advice of Suze Orman and spent one whole month tracking (1) how much income I was bringing in and (2) how much money I was spending. Both numbers floored me.

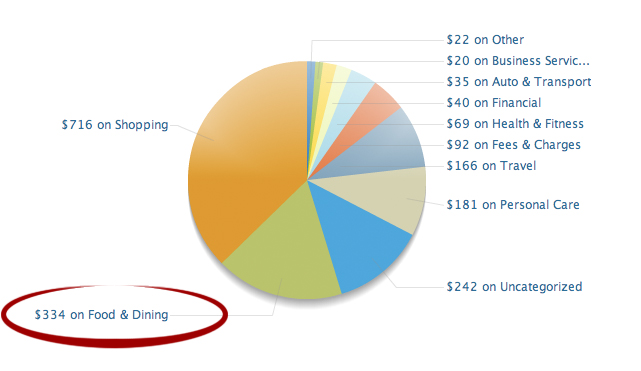

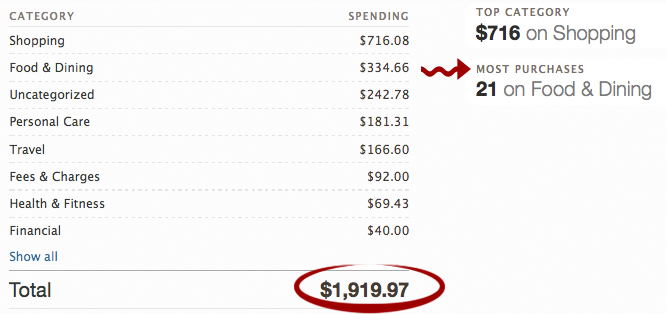

Here's a screenshot of my Mint.com account during one particularly gratuitous month, January 2009.

There's 2 things wrong with this picture. The first is: I DON'T MAKE $1,900 A MONTH!!! The second is: I WAS SPENDING $1,900 A MONTH!!! My heart almost stopped I saw this almost 2 years ago. This is what happens when you own credit cards and don't keep track of what you spend. You can get into a HEAP of financial trouble.

Once I saw this, I immediately switched to a cash only system—if you only use cash, you can't spend what you don't have. Because Mint.com is difficult to use if you primarily use cash, I started doing my money tracking on a simple excel spreadsheet and have been ever since. I write down (or save my receipts) every time I purchase something with cash, and I add it to my spreadsheet at night. Because I started tracking my money, I was able to realize where I was able cut out a lot of ridiculous spending, get a $900 credit card balance down to $380, and save $500 for emergencies in less than 6 months. If you learn nothing else from today's blog post, know that you have to track your money if you want to get a handle on your finances quickly.

Saving 10%

I love Proverbs 22:7 in the Bible which says, "The rich rules over the poor, and the borrower is the slave of the lender" because it is so unbelievably true. If you've ever had your bank account ravaged until an overdraft fee was paid or have had your college purge you from your classes until you paid them your back tuition, then you already know that owing people money is one of the worst emotional and financial positions to be in, EVER. What's even worse than that, however, is having to rely on credit cards, loans, or other debt to get out of a tight pinch because you don't have an emergency savings fund.

Everyone should and can have an emergency savings fund if they commit to saving at least 10% of their total income. This worked phenomenally for me once I realized the power of that word "total", in total income. "Total" means all the money that ever comes in to you, a minimum of 10% of it is going to go into your savings account. Just got paid $500 from work? $50 better go into your savings account. Grandma just sent you $25 in the mail? $2.50 better go into your savings account. Just got a $1000 tax refund check from the government? $100 better go into your savings account. A friend just paid you back the $5 she owed you from last year? $0.50 better go into your savings account. It doesn't matter how large or how small the amount is, the point is all of those "10%'s" really start to add up. If you keep at it and even turn saving into something enjoyable to watch as it grows, you will not believe how much money you can save in a short amount of time. And no-strings-attached money in the bank is always a great foundation to getting a handle on your finances now.

***

I hope these tips are enough to inspire you to get your financial game together, NOW. Understand what your problems are, start tracking your money, and begin to save 10% and your financial life will begin to change in ways you couldn't have imagined. These steps are by no means the only things one must do to get a handle on their finances, but they are the best things you can do *right now* to begin to see some immediate changes.

What inspired you to get a handle on your finances? What steps are you taking now to make the change? Leave you comments below.

.png)