Have you ever been so reckless with you finances that you were too scared to even look at your bank account?

Maybe you had a wild weekend with friends. Or you did some serious, unplanned damage at the mall last week. Then there’s that one bill you meant to pay off weeks ago but you haven’t gotten around to it.

You know you’ve screwed up and you want to fix your situation but you don’t know how.

Girl. I. Have. Been. There!

And since I’ve been there, I can’t let you continue to swipe your debit card knowing you haven’t looked at your account in three weeks. Yeah…I can’t let you go out like that.

Come on, let’s get your financial stuff together. I’ll even help you –right now! Here’s a 5 step plan I’ve put together to help you face your financial fears (because you can’t ignore your bank account forever…):

#1 – Look at Your Accounts

YES! You have to look at your checking account! Come on, what did you think I was going to say? You came here to learn how to get over your fear of your finances, right? Okay then, you gotta do this.

No more ignoring, because ignoring your account for weeks is a ridiculous thing to do anyway.

And I’m *literally* laughing as I say that because I DID IT! I was the girl who ignored her checking account.

For weeks.

After buying a pair of $89 BCBG shoes I couldn’t afford for homecoming week in college.

And you know what? I was also the girl crying on the phone in with her Dad in the middle of the Bank of America lobby (true story), begging him to wire me some money because I had overdrawn my account by FIVE HUNDRED ($500!!!) dollars.

So yeah. I’ve been there.

That’s what ignoring your account will get you. Now be a big girl, open up another tab in your browser and log into your bank & credit card accounts. Yup, pull those bad boys up. Don’t worry, I’ll wait. (*said in my Kat Williams voice*…)

#2 – Find Out How Much You Spend

If you’re anything like I was, looking at your accounts probably just made you a little sick. That’s okay. I’m done with my “tough love” stance for now because you did it. You looked at your accounts! And I really want to encourage you.

Before we go any further, really take in your account — all the charges, all the purchases you are kicking yourself for making, all those late & overdraft fees — and forgive yourself. Do take note of your mistakes so you don’t repeat them, but no need to beat yourself up. What’s done is done and now we’re moving forward.

Okay, so now that you’ve looked at your account, you need to figure out how much you spend. Not what you think you spend, but what you actually spend. You can do this in one of two ways:

Method 1: Walk around with a notebook and write down what you spend for 30 days.

If you’re disciplined, this may work, but if you aren’t willing to write down every single purchase, its probably better you skip this one. Plus, if you start now, you may be tempted to drastically cut your spending having just looked at your account.

While spending less is good and something you probably need to do, we need an accurate picture of how you normally spend so we can make permanent changes.

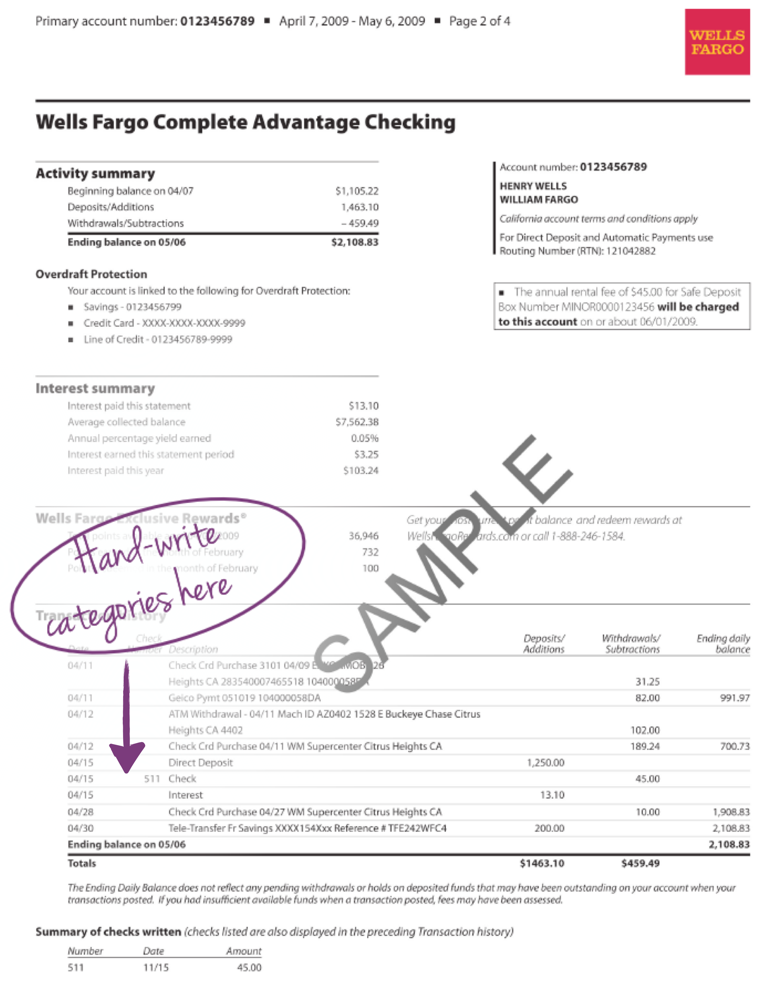

Method 2: Go through last month’s bank statement and categorize your purchases.

This method is pretty straight forward but you’ll need a calculator, some pen and paper, and about 30 minutes to go through everything.

Print off your bank statement and next to each purchase, write the category it belongs to.

So if you see something like:

“Check Card Purchase 10/21 CHICK-FIL-A Atlanta GA”

(Because who doesn’t love Chick-Fil-A???)

…on your bank statement, write “Eating Out” or “Restaurants” or some other similar category name next to it.

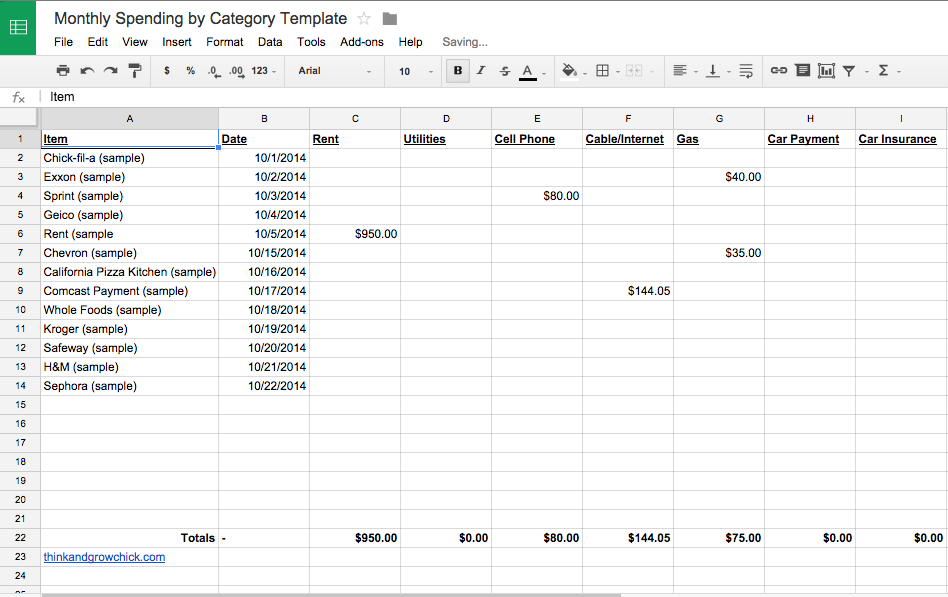

Once you written categories next to EVERYTHING on your bank statement (“Eating Out”, “Rent”, “Shopping”, “Grocery”, etc), add up all the amounts for each category on a separate sheet of paper.

Or, you can use this custom google spreadsheet I made just for you if you’re fancy. 🙂

#3 – List All Your Debts

Remember how I told you to forgive yourself when you looked at your bank account? Get ready to forgive yourself again because now it’s time to figure out how much debt you have.

The only thing worse than being broke is being in debt. So, yeah. This part may be kinda painful. But it must be done! You can’t really face your financial fears until you know what you are dealing with and for most of us (myself included!) debt is a part of that equation. So, onward we go!

Off the top of my head, I suspect you may have four kinds of debt:

1. Car Loan

2. Student Loans

3. Credit Card debt

4. Past due bills/Collections

I’m really hoping you don’t have past due bills or anything in collections but if you do, that counts as debt as well and we have to address it. (Remember, don’t beat yourself up!) Here’s how to figure out the totals for each type of debt:

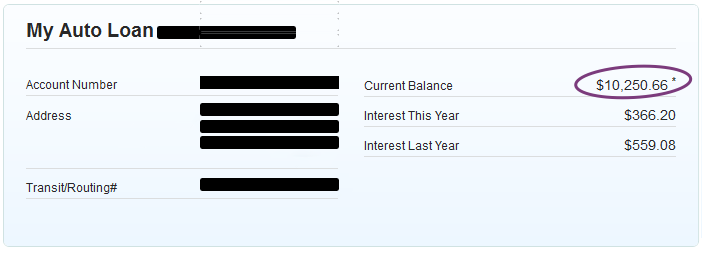

How to Find How Much You Owe on Your Car Loan

Finding out how much you owe on your car should be pretty easy. Most people have their car loan through a bank, which means you should be able to find out how much you owe online. Just log into whichever bank account your car loan is through and navigate to the “car loan” (or “my loans”, etc) tab.

When you get to the right screen, write down how how much you OWE on the car (not just your monthly payment).

How to Find How Much You Owe in Student Loans

Student loans are a little trickier to round-up because (1) you may have multiple student loans across several different lenders and (2) lenders sell their student loan portfolio to new lenders all the time, which means you are probably paying a different lender than the one you originally got your loan from.

Never fear, with a little legwork, you too can find out how much your education cost you!

If you received FEDERAL student loan aid (i.e. not a private loan), you can get a total of all your loans by visiting the OFFICIAL National Student Loan Data System website at: www.nslds.ed.gov

You will need your name, date of birth, social security number, and your 4-digit FASFA PIN (you received this when first applying for financial aid when you were in school) to log into the system.

(Side note: If you don’t have or remember your 4 digit PIN, go to www.pin.ed.gov to get a new one.)

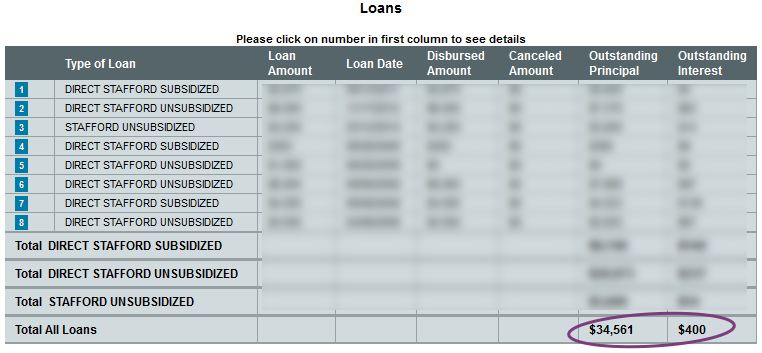

Once you’ve gathered up all your info and logged in, you should see a table that totals all your student loans. Here’s mine:

Now if you have private student loans (i.e. Sallie Mae) in addition to your Federal loans, you will need to log into your loan accounts with those lenders and pull up your student loans.

Once you’ve found all your student loans, write down the TOTAL amount you owe.

How to Find Your Credit Card Balances

*Sigh.* The dreaded credit card balances.

I’m guessing you already know how to find out how much you owe on your credit cards, you just don’t want to.

Remember: (1) we’re big girls now and (2) we FORGIVE ourselves for past financial mistakes! Why? Because we are moving forward. And moving forward means taking a look at those balances.

So you know the drill. Fire up some new tabs in your browser and log into Visa, Mastercard, Discover, Amex (big roller!) and any other credit card account you may have. Write down all the credit card balances you have on a separate sheet of paper and add them up to get the TOTAL you owe.

How to Find Past Due Bills/Collections

Much like with your credit card balances, I suspect you at least know which bills are past due or in collections as the companies you owe will typically send you lots of letters and leave lots of voicemails.

To figure out how much you owe, gather up all those letters you’ve been avoiding (*ahem*) and write down all the companies you owe. Depending on how long you’ve been avoiding past due bills, the balances listed in the letters may not be accurate as you may be racking up late fees and penalties. Because late fees SUCK, you need to get up-to-date balances on all your past due bills right away.

Once you have your list of companies you owe, first see if you can find out your balances by logging into your account online. Cable, utility, cell phone, and other consumer companies typically allow you to check your bill online without needing to talk to anyone.

However, if you owe, say, medical bills or something more obscure, you may not be able to check your balance online which means you will have to call them. I know, I know — call your bill collector?!?! Hey, you have to find out how much you owe. If you don’t have the money to pay right now, then you don’t have the money to pay — just tell them that. The important thing is that you verify your balances. (Also, be sure to ask for a break down of the total as you may be able to negotiate both the original charge and any accrued late fees.)

If an account has gone into collections and you’ve been avoiding it for a long time, there’s good chance it’s on your credit report. You can find out by requesting your free annual credit report at www.annualcreditreport.com, the OFFICIAL free credit report website. I’d also personally recommend CreditKarma.com, as it is a free service that monitors your credit and will alert you when any negative information is added to your credit report.

Once you’ve found out the up-to-date amounts you owe in past due bills, write it down.

#4 – Find Out How Much You Make

Now it’s time to figure out is how much you make.

Yup! No more spending recklessly if you don’t even know what your income is every month!

If you get a regular paycheck every week or every two weeks, then this should be easy. Just add up your paystubs for last month and write down how much you made. If you don’t have your paystubs on you but you always deposit your paychecks (or if you get direct deposit), you can search the bank statement you just printed out for your paycheck deposits.

If you are a freelancer or otherwise work for yourself, go through your bank statements and add up all the deposits related to your income. In fact, I would recommend finding your average income for the last THREE months if you work for yourself, as freelance income may vary month to month.

Once you’ve added up all your income for the month (or last three months if you’re self-employed) write down your monthly income. Also note how frequently you get paid — every month? Every two weeks? Every week? Write that down too.

#5 – Make a Plan Going Forward

You’ve looked at your accounts. You know how much you’re spending. You know how much you owe. You know how much you make.

You are doing really good, so hang in there! We’re almost done.

The only thing left to do now is make a plan going forward. Now that you’ve faced your financial fears and you know what you know, what changes are you going to make going forward?

To help you map out your new financial future, I’ve created my Financially Fearless Worksheet for you to print out, fill in, and sign. This will help you summarize your financial picture and more importantly, make a plan going forward:

This worksheet contains three (3) pages to help you walk through the above 5 steps. Once you follow the steps above and fill out this worksheet, you will officially be FREE from your financial fears, guaranteed. Click here to download.

Feel free to show off your completed worksheet on Instagram, Twitter, and Facebook using the hashtag #IamFinanciallyFearless. (#IaintNevaScared works too!)

Bonus

I get tons of emails from women who need help getting their finances in order. If you still need help with things like setting up a budget you can actually stick to, creating a savings plan, etc, you should sign up for my email list. Right now I’m working on a training product that will show you how to organize your finances in a way that leaves you confident and clear. If you want upcoming sneak-peeks and free samples of the product before its released, sign up for my newsletter here.

Photo Credit (top): aag_photos

Related Articles

< Back to all blogs

Have you created your vision board yet? Written out all your goals? Found that perfect planner? Bought that perfect little notebook with the world most inspiring quote written on the cover?

.png)